Interest rate cuts by the U.S. Federal Reserve are becoming less likely in the near term, as economic indicators and geopolitical factors, like an act of aggression from Israel and the US towards Iran, weigh on monetary policy decisions. Following a steady effective federal funds rate of 3.64%, market expectations for a reduction have dwindled significantly, with only a 47% chance of a rate cut through June, as noted by market analyst Mike Zaccardi.

Citibank has commented on the situation, stating that geopolitical developments, such as tensions relating to Iran, are not expected to have a significant effect on the Fed’s policy rate plans. The bank highlighted that modest upside risks to inflation, combined with less favorable financial conditions, will likely impact rate decisions, according to insights shared by Michael Derby.

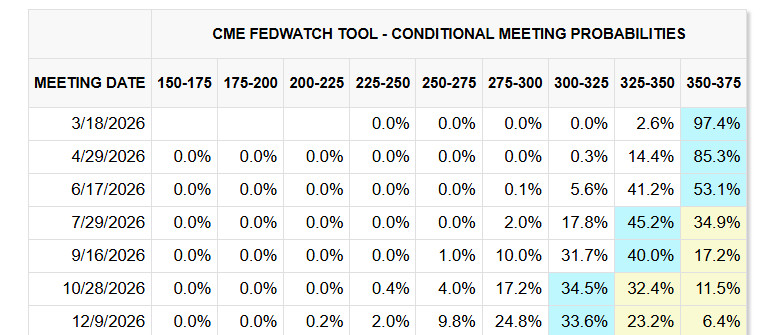

Meanwhile, analysts are closely monitoring inflation trends, particularly following a higher-than-expected Producer Price Index (PPI) report. According to a gauge by CME FedWatch, there is a 96% likelihood that the Fed will maintain rates in March rather than initiate cuts, as discussed by Math Democrat on social media.

This mixed outlook is compounded by ongoing trends in risky asset investment, which typically rise during periods of lower borrowing costs. However, the current economic environment, characterized by stable oil prices and the effective federal funds rate remaining unchanged, dampens expectations of imminent cuts.

The impacts of these dynamics are being felt across various asset classes, as evidenced by the performance of 10-year U.S. Treasury bonds, which recently fell below their weekly moving average support band. With sustainable growth and inflation concerns at play, the nature of U.S. monetary policy remains a key focal point for investors in the upcoming months.